xTuple keeps it simple – many small to medium-sized businesses don’t consider ERP because they think it’s too complicated.

We believe in KISS (keep it simple & straightforward), so simplicity is baked into our software design and we avoid unnecessary complexity.

Digital transformation should be simple – optimize your data to achieve end-to-end visibility so that you know where your time and money go, and how to improve your business processes.

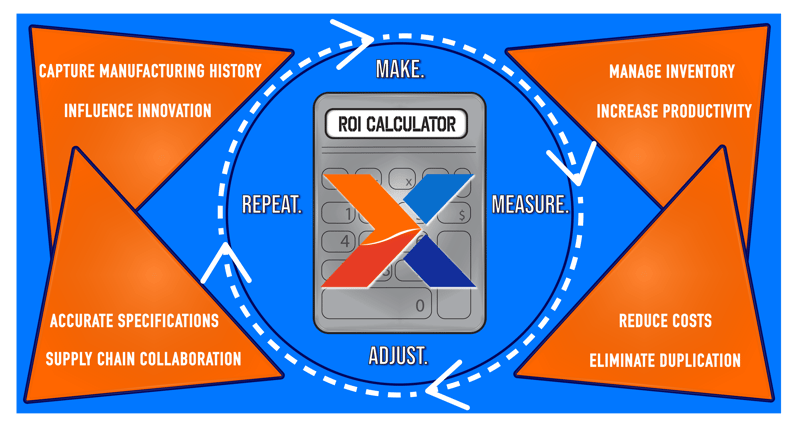

We developed a super simple return on investment (ROI) calculator – you don’t need an Excel spreadsheet or a scientific calculator, as a business owner, or a shop foreman, the information you need to use our ROI Calculator is already in your head.

Plug your information into our ROI calculator and see how, even with minimal inputs and conservative improvement percentages, xTuple ERP can have a significant impact on the following areas of your business:

Contact

xTuple

A CAI Software Company

24 Albion Rd, Suite 230

Lincoln, RI 02865

+1-757-461-3022

About

"xTuple" (verb) — to grow; to increase exponentially. Our mission is to help manufacturing and inventory-centric companies use management software and best practices to grow their business profitably.